Photo by Michael Longmire on Unsplash

I suspect that most people believe that the primary job of a bank is to look after their cash.

Deposit your money and, at any point in time, you can rock up at a branch or a hole in the wall and receive your cash up to the amount that you put in, minus a few fees.

The reality is that banks only provide a haven for our cash because it allows them to leverage the money held into investments. They borrow against their available capital and invest funds into a wide range of assets that they expect will yield more than what they’re giving you for the privilege of looking after your money.

It’s a fantastic financial model.

It’s the reason that having conquered the world of futures trading, capital gains, and hedge funds, Bobby Axelrod, the megalomaniac character in the Stan thriller Billions, played by Damian Lewis, decides he wants to become a bank.

Essentially it’s a license to print money.

Banks are always looking for assets that will yield investment returns in the shortest space of time. Their mantra, indeed their requirement under the law, is to profit, and they are ‘in the pound seats’ to do it, literally.

They have the scale and capacity to invest in projects that your average Joe couldn’t dream of, from skyscrapers to industrial plants, freeways, and airports. The kinds of investments that require tens to hundreds of millions of dollars to see them to fruition.

Banks have the advantage of using other people’s money and the advantage of scale. They make huge sums from investments that yield high returns for long periods, partly on the fact that no one else can invest in them.

And so it is and has been.

The banks make money, but the projects they fund often deliver utility.

Banking externalities

It is not always good.

The pursuit of profit is relentless and ruthless.

Goldrush mentality attracts the most ardent and most skilled as well as the opportunist. Money gives banks the very best people with a sharp mind and a ruthless attitude. They quickly find the best ways to reduce costs and maximise returns.

No surprise that banking can support projects that have severe externalities and direct impacts on the environment. Recall an externality happens when the cost of an activity is not absorbed but shipped out. The commons are excellent dumping ground because no one person or entity gets hit with the liability.

Capitalism degrading the environment is profound. Development has to happen, but it becomes pointless if humanity has no safe place to live.

So who is to blame?

The reality is that we, the people, want roads, skyscrapers, and industrial plants that deliver raw materials for all of the stuff we want to buy.

We are the ones that live in large houses with more bedrooms than you could ever need, more luxury than you could ever really afford. And yet, everyone wants a better life, and it is forever the human condition to want betterment.

In other words, the consumer is ultimately responsible.

Instead of blaming the banks, what if we blame the consumer?

Maybe get consumers, us, to give up our desire for stuff, our emotional and mental drive to better ourselves and provide for our families. Quosh those innate biological feelings to make more that is in all of us.

Well, good luck with that one.

Perhaps there is a compromise position where both individuals and the finance community begin to work together to look long and prosper.

Currently, we do this through regulation.

Governments curtail the riskiest financial behaviours through legislation limiting the amounts of money banks can borrow, their financial ratios, and their ability to exploit customers, in itself a significant ongoing task.

Governments are in a difficult position. They see growth as a political necessity and are reluctant to curtail development activity or the banks that finance it. Yet, all the while, development activity is damaging the planet.

If we can’t blame ourselves or the banks for doing what we want them to do, humanity has a problem.

People’s choice

We do have a choice.

We can accept that consumption and more-making has an impact and try to do something about it. Even a little is better than doing nothing. Light bulbs, anyone?

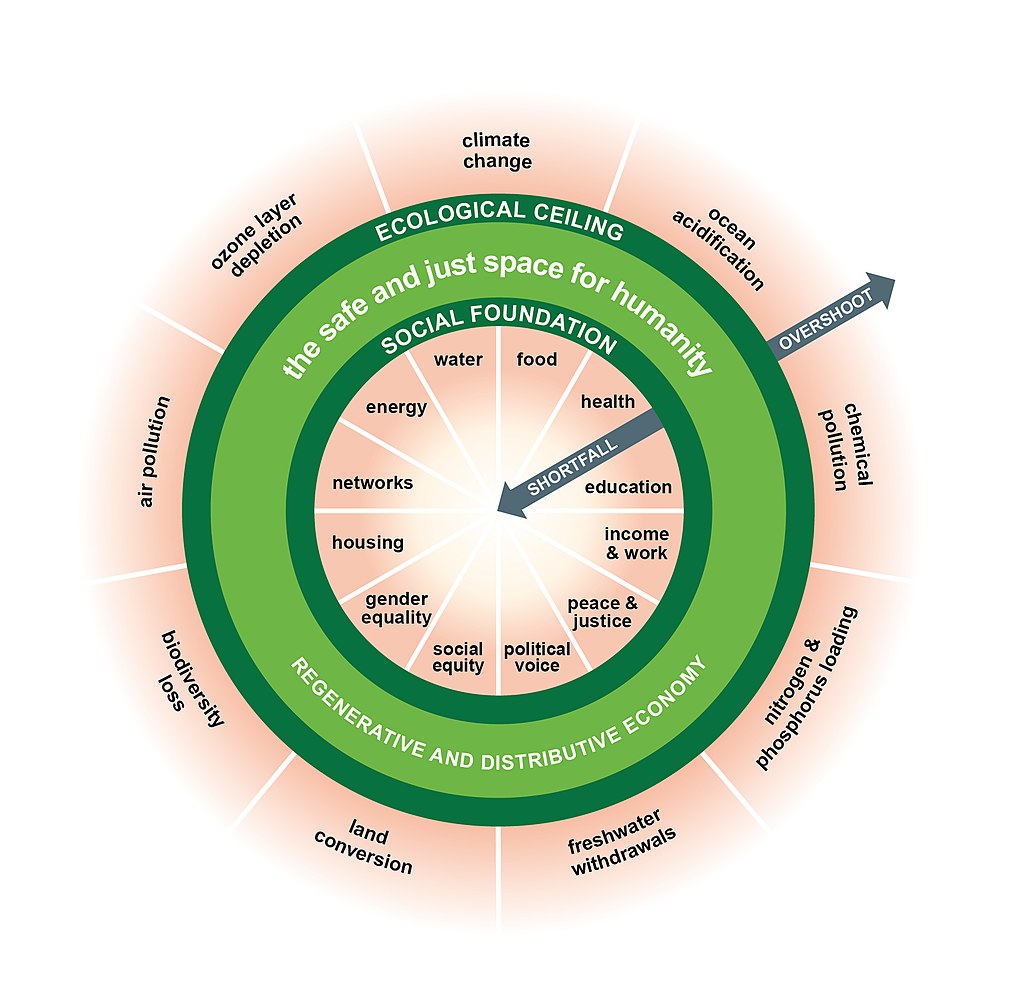

But fiddling just puts off the inevitable. Instead, something dramatic is needed. The doughnut, perhaps?

Alternatives to historic capitalism exist, and many of the options are maturing nicely.

For example, ‘cooperative enterprises’ where workers make the major enterprise decisions rather than boards of directors selected by shareholders. This alternative is called economic democracy.

Only this is not a million miles away from what we already have. The people choose, but this will not guarantee decisions in favour of anything other than the people.

Robin Hahnel’s book Of the People, By the People: The Case for a Participatory Economy describes the participatory economy where all citizens, through the creation of worker councils and consumer councils, deal with large-scale production and consumption issues without the need for appointed representatives. The participatory economy is the origin of the Green New Deal, a package of policies that address climate change and financial crises.

A participatory economy is different. Imagine the circus of state and national politics banished to the bench.

Doughnut economics is an economic model proposed by Kate Raworth that combines planetary boundaries with the complementary concept of social boundaries. Look after everyone and the planet.

Doughnut economics is different too.

And these are just three of the many alternatives with potential.

What do the alternatives require of us?

Most of the alternative economic systems require a shift in responsibility.

It would be on us, not the banks or the government or the unscrupulous developers. We will all have to step up and understand the consequences of our choices.

The banks would continue to do their thing on our behalf; only we would be responsible for the consequences of what they do.

And so we get to the rub.

Capitalism has delivered growth and, on average, betterment for humanity. Only it comes at an uncomfortable cost. And the only way to pay back that cost is to take responsibility for it.

Are banks bad? No, they are a caricature of our abdication from personal responsibility.

Please like or share or comment. It helps me heaps, thanks.